Senior Product Designer @ TWISTO / ZIP

Nov 2017 - Aug 2022

One designer. Four teams. Scaling Twisto from early-stage BNPL to acquisition by Zip

$0M

$0M

Acquired by Zip in 2021

0M+

0M+

Customers

0K+

0K+

Merchants on the platform

Rebuilding the core experience around the two things users actually needed

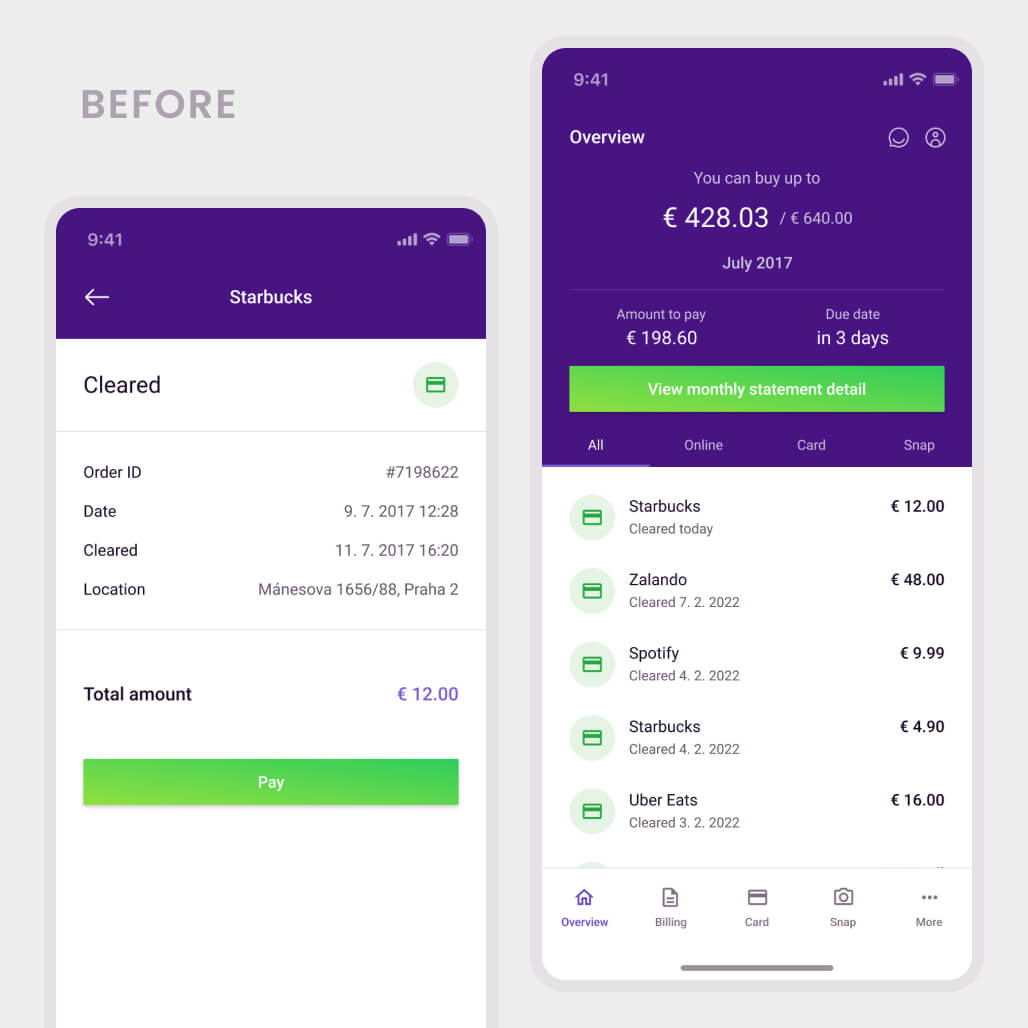

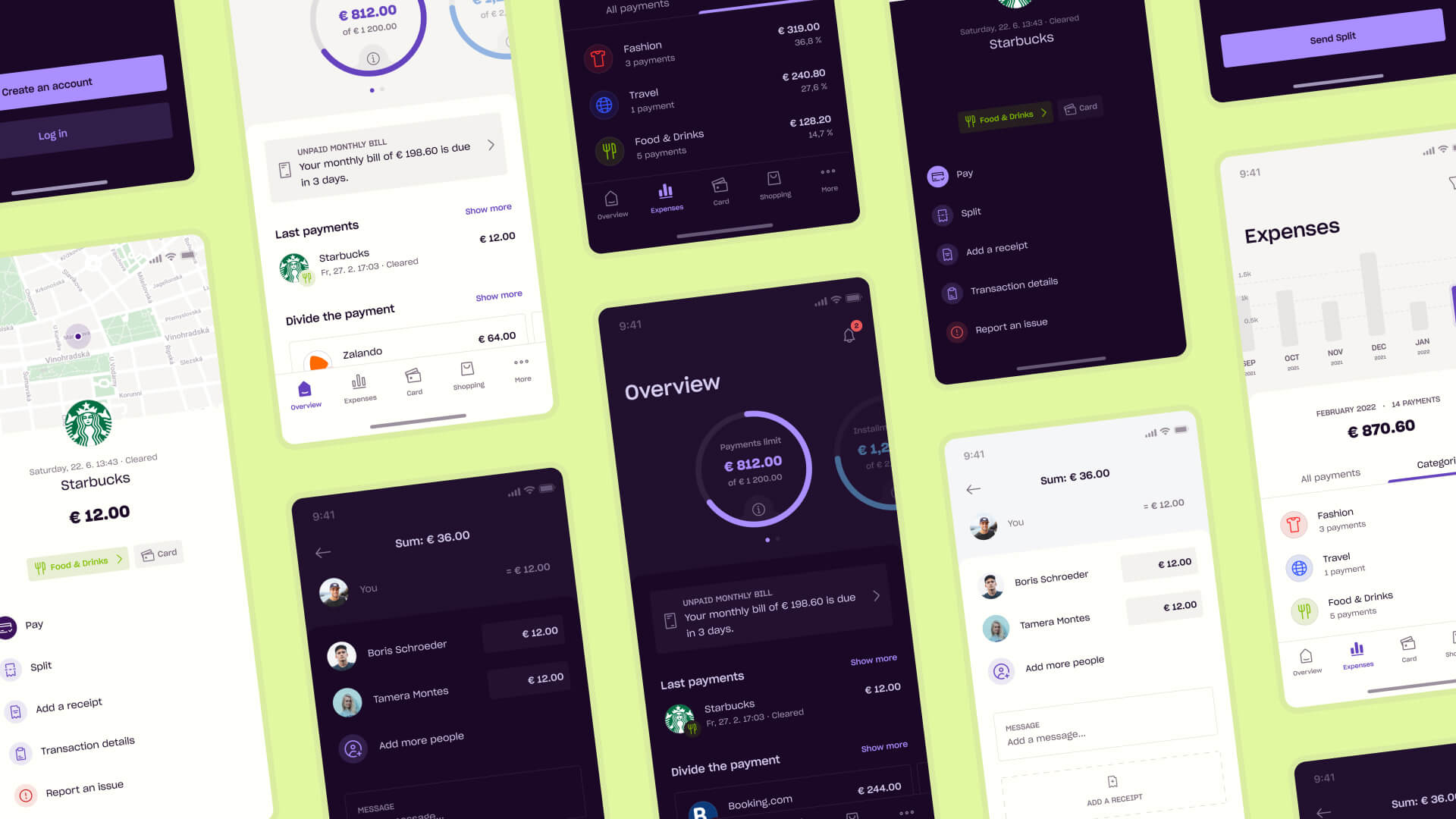

The product lacked hierarchy and made common tasks harder than necessary. Checking available credit and reviewing transactions, the primary reasons users opened the app, were buried.

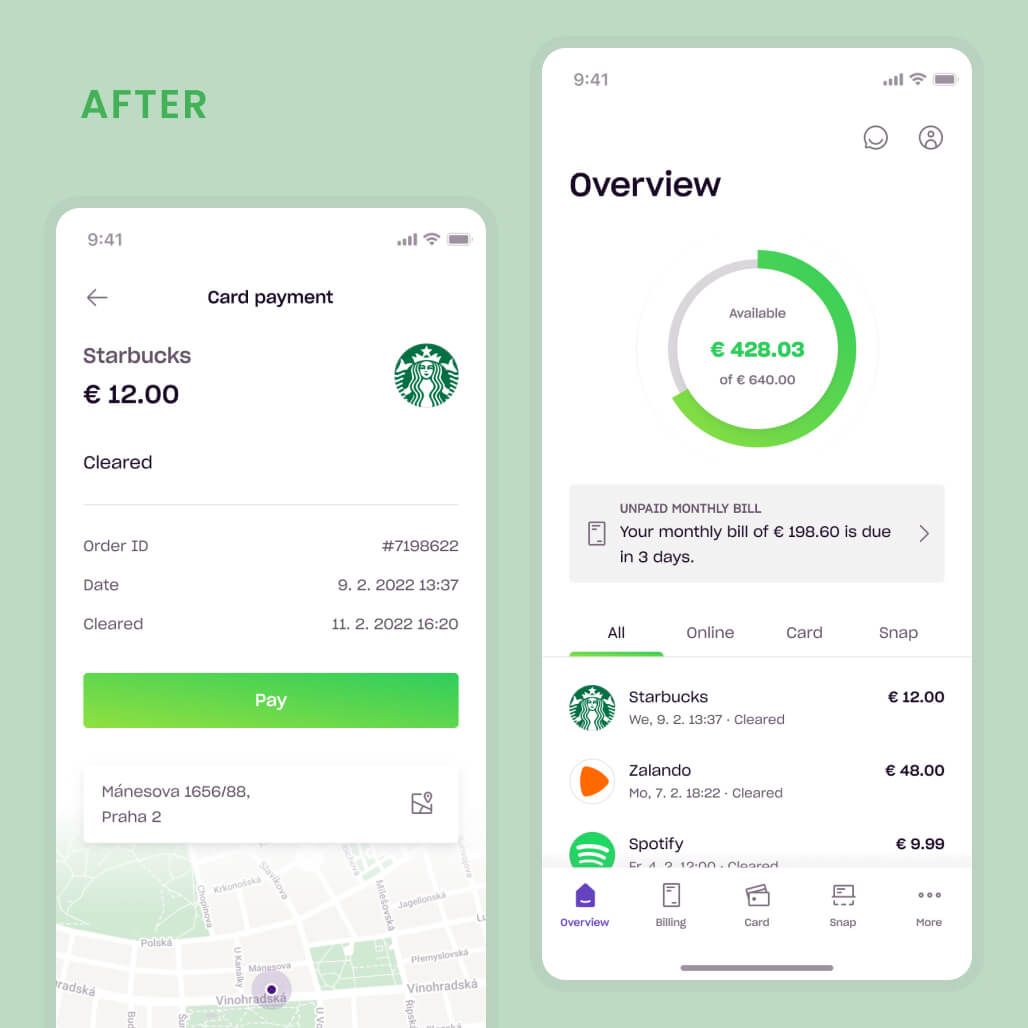

User research pointed clearly in one direction. Credit moved to the centre, transactions became easier to scan, and billing was condensed into a single summary. The redesign was not complex, but getting the fundamentals right created a stable foundation for everything that followed.

Onboarding rebuilt as a modular flow

The original onboarding flow asked for everything in two screens. It looked like a bank form. Drop-off data showed where users left, but not why. Usability testing revealed users did not understand what they were signing up for or why each step was needed. I redesigned it as a progressive, conversational flow, one input at a time, with plain language and a clear reason for each step. Completion improved and drop-off became easier to diagnose.

The key decision was modularity. Each step was independent, allowing us to adapt onboarding for different KYC and AML requirements when expanding into Poland and Turkey without rebuilding the flow.

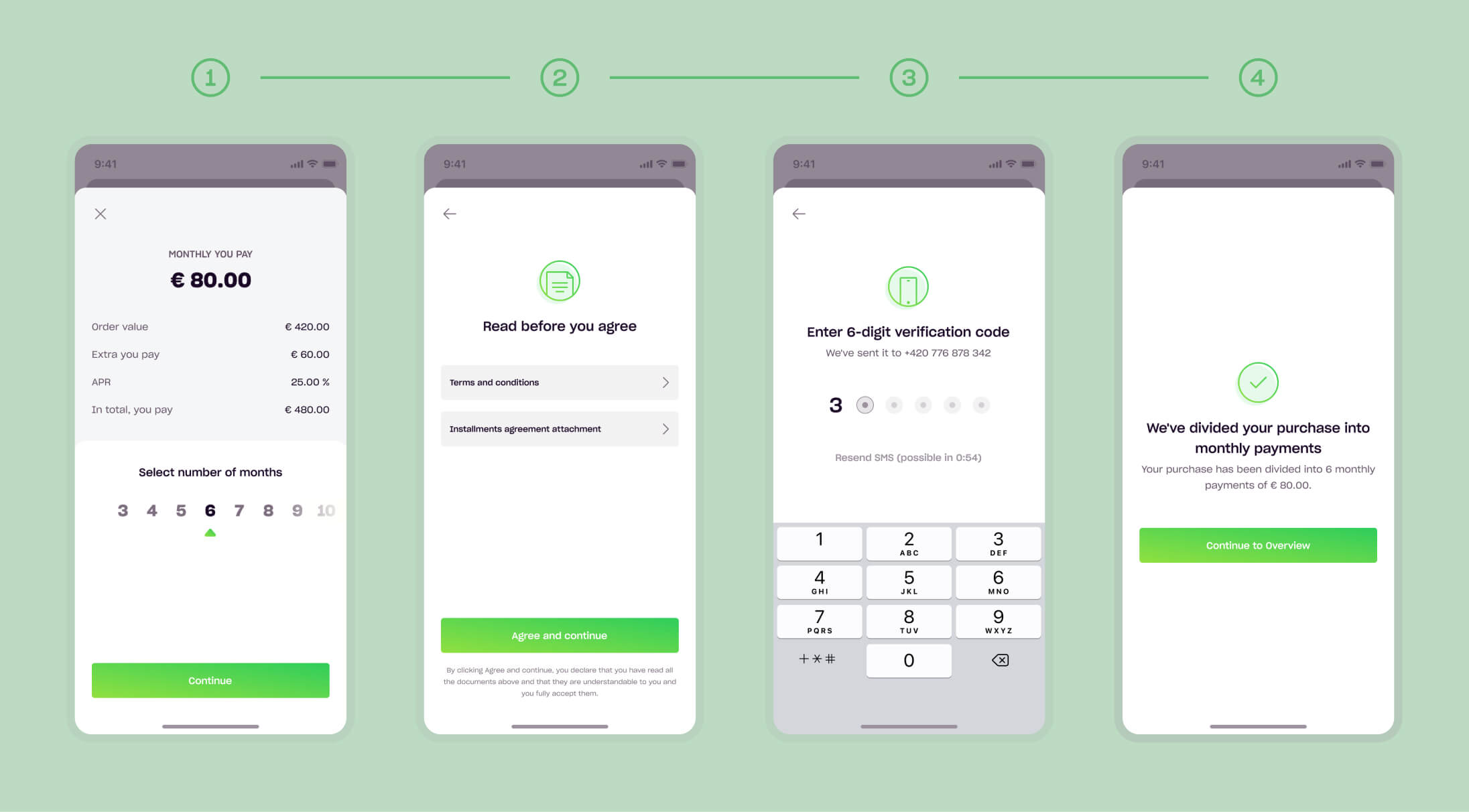

Instalments were a revenue opportunity blocked by perception

Instalments were underused because users associated them with debt. I ran A/B tests across copy, entry points, and timing to identify where resistance was strongest. Instead of separate flows, I combined Pay in 3 and longer instalments into a single experience. Leading with Pay in 3 at 0% APR lowered the barrier to entry and increased instalment adoption across both markets.

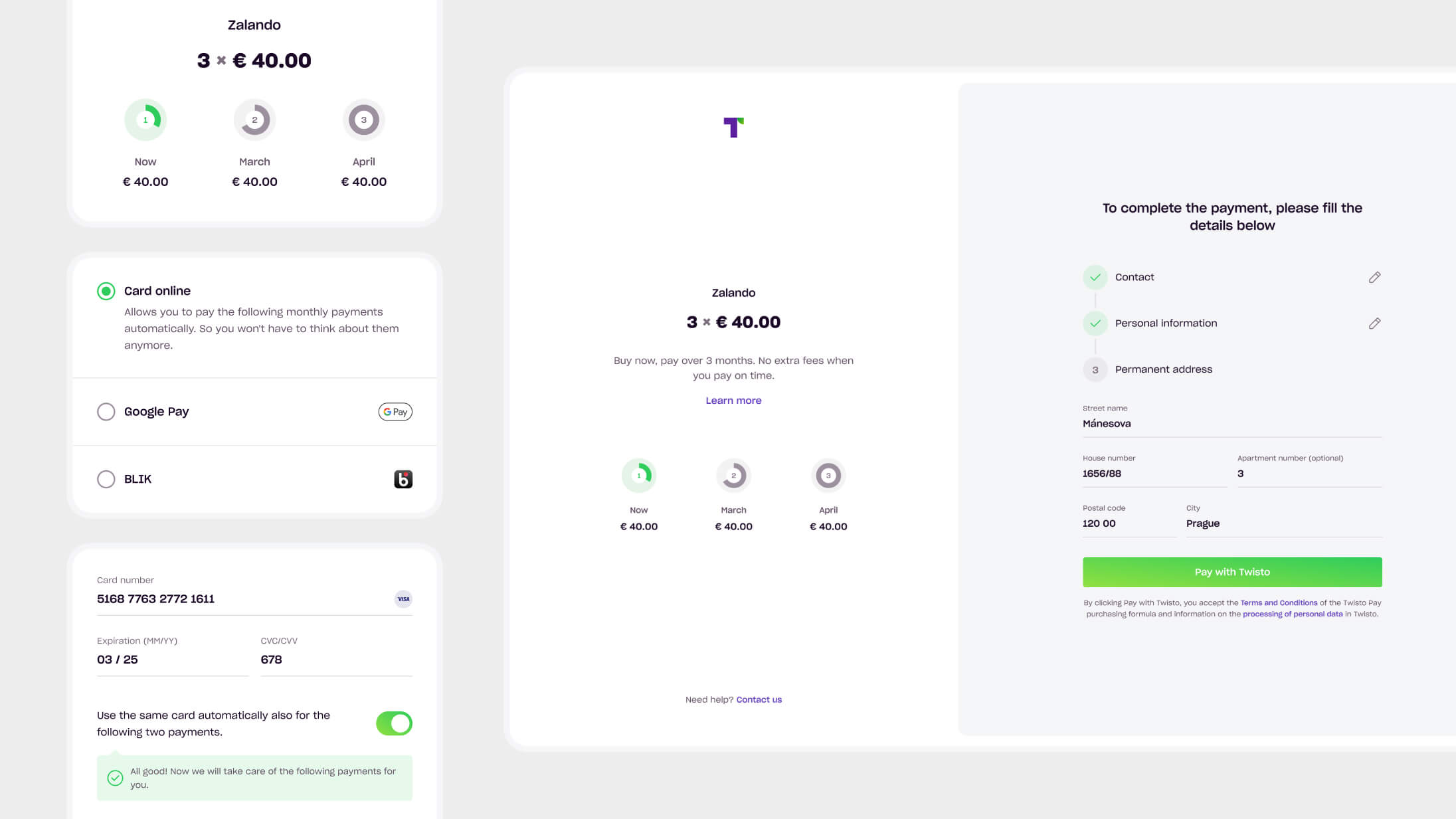

Owning checkout enabled recovery flows that reduced drop-off and improved conversion

Before building our own payment gateway, checkout relied on third-party integrations. We had limited visibility into failure points and no way to recover users. Owning the checkout changed that. I mapped the full journey and used transaction data to identify where users dropped, aligning product, engineering, and risk around recovery opportunities.

We introduced fallback paths that kept users moving. Users with insufficient credit could switch to instalments, users flagged for checks could complete them inline, and users unable to pay with Twisto could continue with another method. Each path reduced the chance of losing a user at the final step.

Design system supported two brands through acquisition without fragmenting the product

Following the acquisition by Zip, Czechia moved toward Zip branding while Poland remained Twisto. Two markets, two brand identities, one system.

I introduced token-based theming, removed legacy components, and resolved accessibility issues, particularly around colour contrast. This allowed both brands to coexist without maintaining separate codebases during a period of significant business change.